Across India and the world, millions of people are in work, yet work alone has not guaranteed financial security. For low-income workers, a job provides income but not always stability, a buffer against emergencies, or the financial tools that allow households to plan ahead. The gap between being employed and being economically secure is wide, and for many workers it is not narrowing. Budget 2026-27 treats financial inclusion as a foundational condition for growth - economies cannot expand their productive base if large sections of the population remain outside the formal financial system, unable to access credit at reasonable rates, or weather income shocks without falling back into debt.

At the household level, access to formal credit and savings tools allows families to invest in housing, healthcare, and education, and to absorb shocks without losing ground. At the workforce level, financial fragility has a direct cost. Workers managing informal debt, cutting essentials, or anxious about making it to the next payday are less focused and less productive. Research consistently shows that financial stress reduces cognitive capacity and increases absenteeism costs that show up in firm performance as much as in worker wellbeing. Research¹ found that financial stress reduces cognitive bandwidth, making decision-making harder. In one study, farmers struggling with financial strain performed significantly worse on cognitive tests than when financially stable, equivalent to the effects of losing an entire night’s sleep.

In the same uncertain global environment that makes worker health a strategic concern, financial fragility at the household level carries costs that extend well beyond the individual — into firms, supply chains, and the domestic economy's capacity to absorb shocks."

what the budget does and does not account for?

The Budget makes strides in moving financial inclusion beyond opening bank accounts toward usable credit for those at the bottom of the pyramid.

Upgrading Micro-Entrepreneurs: The revamp of the PM SVANidhi scheme extends loan periods, increases tranches (up to ₹25,000 for the second cycle), and introduces a UPI-linked RuPay credit card with a ₹30,000 limit. This gives street vendors flexible liquidity to manage daily shocks. Similarly, introducing credit cards with a ₹5 lakh limit for micro-enterprises provides much-needed working capital.

Solving the “Thin-File” Problem: The introduction of the “Grameen Credit Score” addresses the invisibility of rural and gig workers who lack formal credit histories and are therefore excluded from bank lending.

Last-Mile Delivery: Expanding the India Post Payment Bank to offer doorstep banking and EMI pickup services reduces geographical friction that keeps rural workers out of the formal banking system.

Credit is often seen as the main way to include people financially, but taking on debt does not make workers more resilient. The Budget does not offer clear ways for vulnerable workers to build emergency savings. It also assumes that providing access to digital tools like UPI-linked credit cards will lead to widespread use, but data shows this is not the case. Owning an account or a digital tool does not necessarily translate into usage for mean workers, especially women. Many face barriers like fear, low digital literacy, or lack of control over their accounts. While most Budget schemes focus on business growth, blue-collar workers often end up in debt just to get by between paydays, especially when unexpected emergencies come up.

what we’ve seen in practice

Our work with low-income workers shows that the workplace could be one of the most effective places to address financial fragility. Field data from our work shows that almost all formal-sector women workers have bank accounts, but they rarely control them. Accounts and UPIs are often linked to their husbands’ or children’s phone numbers. As a result, 85% of their cash flows are handled in physical cash, and 80% of their savings go into informal channels such as chit-funds rather than formal banks. Over 60% of their loans come from informal social networks. Fear, lack of trust, and limited autonomy prevent the meaningful use of formal financial products.

Worker Financial Diaries: To bridge the digital trust gap, we introduced a digital budgeting app. Workers tracked daily spending and realised that 38% of expenses went toward non-food items. This awareness enabled them to cut unnecessary costs and increase savings. Interacting with the app in a structured workplace environment also built confidence, with many women purchasing smartphones and using ATMs independently for the first time.

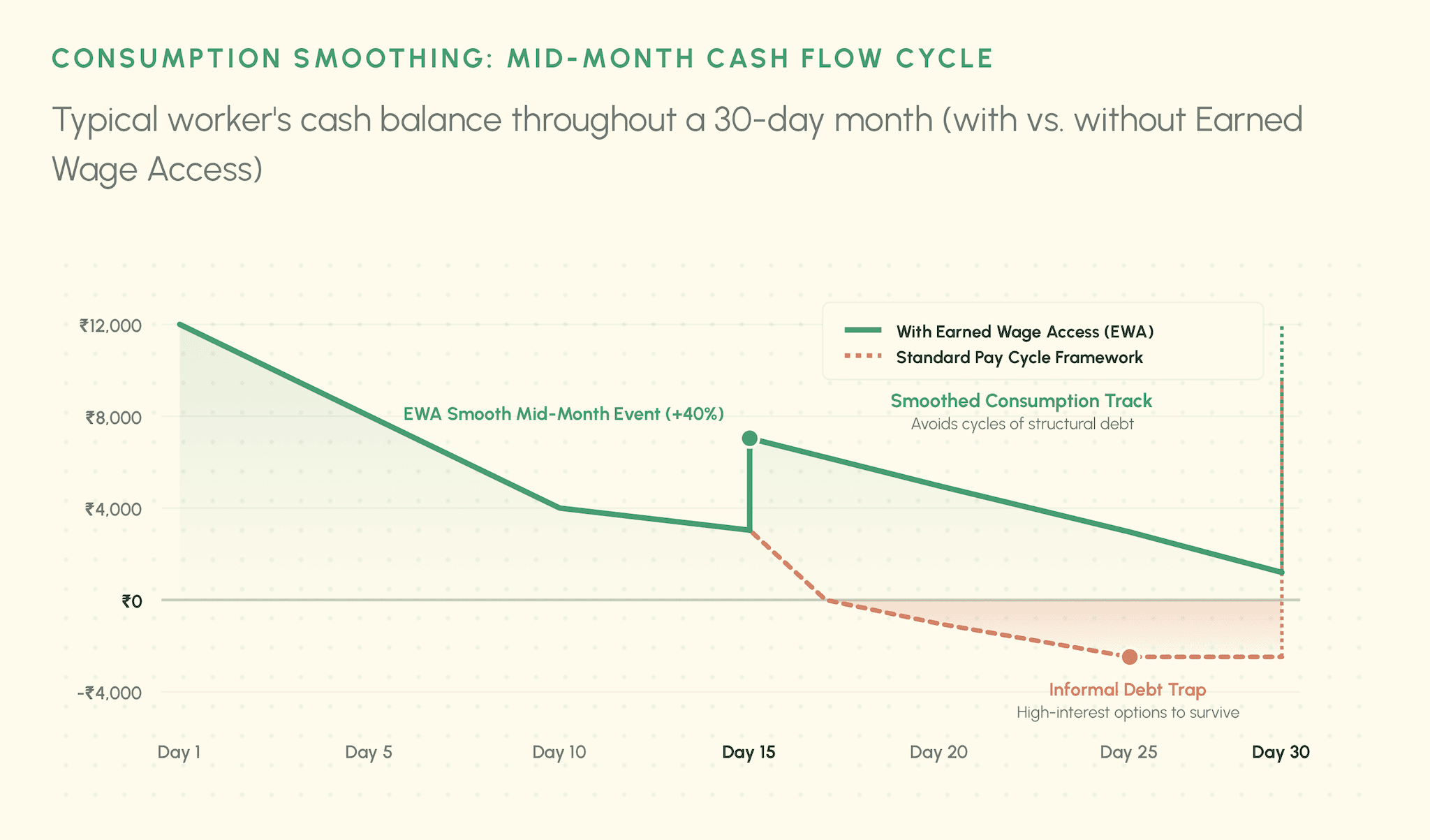

Earned Wage Access (EWA): To prevent workers from running out of money before payday and to address the mid-month cash shortage that often leads them to high-interest lenders, , we piloted an Earned Wage Access tool allowing workers to withdraw a portion of already-earned wages before payday. Informal borrowing dropped by 33%, difficulty in making ends meet fell by 32%, and worker productivity increased by 8%. Notably, 40% of early withdrawals were used to repay existing loans.

financial security is the foundation of good jobs

India has built a robust infrastructure for financial inclusion. Initiatives such as Jan Dhan, UPI, the Account Aggregator framework, and the proposed Grameen Credit Score are transforming basic access into dynamic, data-driven credit for underserved borrowers.

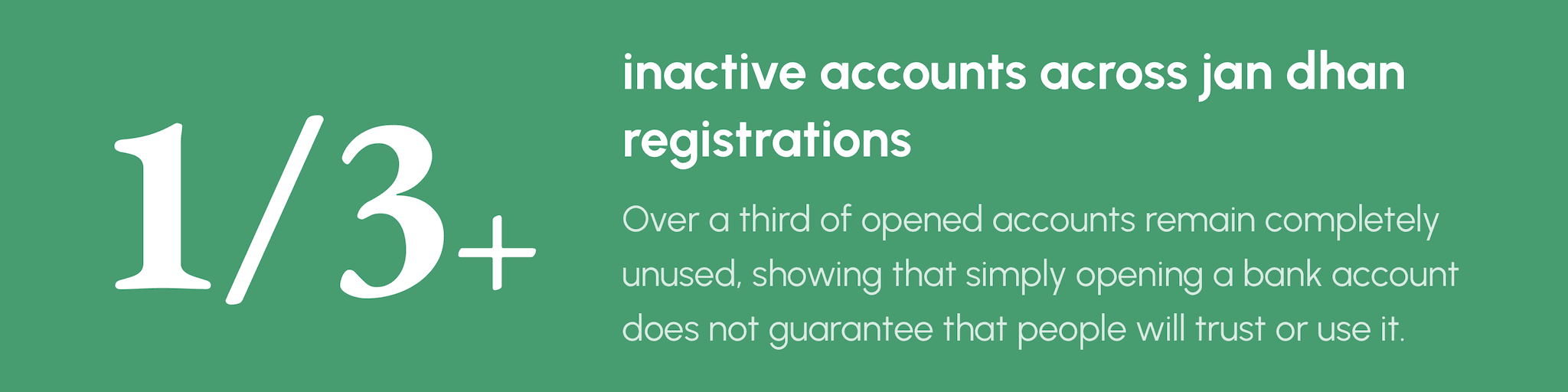

But having the right infrastructure does not always mean people use it in a meaningful way. More than a third of Jan Dhan accounts are inactive, and many formal tools are still not widely used, especially by women who face social barriers and limited decision-making power. The real gap is about trust, personal agency, and creating the right conditions for people to take part.

If resilience is the goal in an uncertain global environment, household financial stability must be treated as a part of economic infrastructure. Workplaces can play a catalytic role by introducing structured support, troubleshooting, and practical tools such as earned wage access and automated savings. When this trust gap is bridged, workers gain financial stability, families avoid debt traps, and businesses see measurable improvements in productivity and retention.

Empowering workers to build financial resilience is foundational to good jobs and stronger, more competitive businesses.

related content

blog

why high turnover persists in retail — and why it matters now

Team GBL

6 mins

blog

budget 2026–27 and the next frontier of financial security

Parridhi A

6 mins

blog

making sexual and reproductive health training work in factories: lessons from the shopfloor

Murchana Nath

7 mins